|

|

|

News from Around the Americas | May 2005 News from Around the Americas | May 2005

A New Way To Send Cash

Mary Lou Pickel - The Atlanta Journal-Constitution Mary Lou Pickel - The Atlanta Journal-Constitution

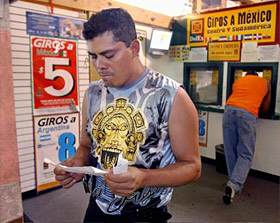

| | DeKalb resident Juan Carlos Zuniga checks his receipt after sending money to Mexico via the Dolex Dollar Express system. He has a bank account but says 'it's easier this way.' (Photo: Kimberly Smith/AJC) |

Enrique Frias went straight to the money agent at Plaza Fiesta mall on Buford Highway and sent $150 to his son in Mexico.

Within 15 minutes, the money arrived in the rural town where the boy and his grandmother live.

"They're throwing a party," Frias explained.

The DeKalb resident paid Western Union $15, or 10 percent, for the convenience. He got a so-so exchange rate.

Sending money from the United States to Mexico is big business. Mexicans living in the United States sent about $16.6 billion last year back to their homeland. That figure is expected to climb to $20 billion this year and an estimated $40 billion by 2010.

But transaction charges, such as the $15 fee Frias paid to send funds to his son, can be steep.

Mainstream banks, meanwhile, which have only an estimated 3 percent to 4 percent of the remittance business, are eager to capture more of it.

That partially explains why officials from the Federal Reserve Bank are touring several cities around the country, touting their fledgling "Directo a Mexico" program, which aims to turn the process into a cheap commodity.

U.S. banks could charge customers as little as $4 per transaction and still make a profit, the Fed says, since it costs the Federal Reserve only 67 cents to send the money electronically to Mexico's central bank. The "Directo a Mexico" exchange rate also is very favorable.

Bankers see this as key to getting to their ultimate aim — to sign up more Mexican immigrants as long-term and more profitable customers.

More than 20 U.S. banks have already signed up for the program as interest increases, said Fed officials, who, along with representatives of Mexico's central bank, were in Atlanta on Thursday to discuss it.

Still, they cautioned, there are hurdles to overcome. Regulatory issues, such as complying with the USA Patriot Act, present one obstacle to bringing more immigrants into the banking system, said Juan Sanchez, the Fed's Atlanta community affairs officer.

That could impact each bank's policies regarding what kinds of identification they're willing to accept before allowing a customer to open an account, he told the small gathering of bank executives who assembled at a downtown hotel Thursday.

In most cases, banks will ask for a picture ID, such as a government-issued passport or driver's license. The Mexican government, through its consulates, also issues what's known as the "matricula consular" ID card.

And while a few hundred banks nationwide accept them, immigrants can still run into snags because most financial institutions require a Social Security number from a would-be customer to check that person's credit history.

There also are fears on the part of some immigrants that they might be deported, mistrust of the banking system, and cultural and language barriers, Sanchez said.

2001 agreement

Still, the Fed is forging ahead with its "Directo a Mexico" program. The program is a result of the 2001 "Partnership for Prosperity" agreement between President Bush and Mexican President Vicente Fox.

The two countries agreed to establish an efficient system for electronic payments between U.S. and Mexican banks.

"The Latino population is constantly growing," said L. Leighton Alston, chief executive of West Georgia National Bank in Carrollton. He was among the executives who attended Thursday's meeting. "It's a market that's very underserved in the state of Georgia."

West Georgia National Bank hired bilingual employees and has made a priority of catering to Spanish-speaking customers.

"We have people driving 40 to 50 miles to bank with us because we can communicate with them," Alston said.

Last year workers in the United States sent $32 billion home to Latin America, according to the Inter-American Development Bank. Immigrants in Georgia sent home $947 million. That's more than any other state in the Southeast except Florida.

The growth of remittances in Georgia is "tremendous," said Fernando Jimenez-Ontiveros, an executive at the Inter-American Development Bank. "Migrants go where the jobs are," he explained. "Other than Florida, Georgia is the Southeast's migration hub."

Small transactions

While important, the remittance market is not sexy. The money is sent in dribs and drabs of $100 to $500.

The average remittance to Mexico was $365, according to 2003 figures from the Pew Hispanic Trust. The average cost to send that money was $16.

A few years ago, bankers started to realize the money transmittal market to Mexico was in the billions.

"Everyone said, 'Holy cow! That's a lot of money!' " said Larry Schulz, the Federal Reserve Bank of Atlanta's vice president of international retail payments. He helped create "Directo a Mexico."

The largest players in the money transmittal market are still companies like Western Union and MoneyGram, which have a loyal following and can distribute the money in thousands of mom-and-pop shops throughout the world.

There's no need for a bank account with Western Union, said Drew Edwards, founder of El Banco de Nuestra Comunidad in Roswell. Recipients can go to an agent in Mexico, show their IDs and say the secret password like "My dog is green," and they'll get their money, Edwards said.

Most immigrants conduct their everyday business outside the banking system in a cash economy where they have no credit and no identity. With post-Sept. 11 fears of terrorism and tighter banking controls, bringing immigrants into the banking system would be a positive step, proponents say. It would clarify the identity of those sending money abroad.

Large U.S. banks have entered the money transmittal market with mixed results. They offer accounts with ATM-like cards that recipients use to pull money out of the sender's account.

Edwards tried this approach, too.

"It's the cheapest way to send money, and we can't get anyone to use it," he said. "Down there, mama isn't near an ATM and she doesn't want to use it. She wants to go down to her butcher shop where she feels comfortable and pick the money up there."

The Fed offers service to 26 Mexican banks with thousands of branches. It already sends 23,000 electronic payments per month to Mexico, mostly Social Security checks that retirees down there have earned, Schulz said.

In July, the Fed's payments will take one day to arrive, as opposed to the current two-day wait. And through a series of agreements with BANSEFI, a Mexican government-owned bank, the Fed will be able to electronically zap payments to a network of about 1,000 credit unions this fall, Schulz said. That will bring the service out to more rural areas.

Raul Limon, president of Dolex Dollar Express, saw the money transmittal business changing six to seven years ago and foresaw it would turn into a commodity. The major difference between companies now is the exchange rate, Limon said.

DeKalb resident Juan Carlos Zuniga, 37, paid $5 to Dolex at Plaza Fiesta mall recently to send $100 to the mother of his son back in Guanajuato, Mexico. The glass installer said he regularly sends money every 15 days. He even has a bank account here but hasn't bothered to figure out how to use it to send money.

"It's easier to send this way," Zuniga said. "You get used to it."

Staff writer Péralte C. Paul con-tributed to this article. |

| |

|